From Operational Efficiency to Net-Zero Aviation: A Singapore Airlines ESG Analysis

SIA’s ESG approach reflects a shift from structured reporting to transition-focused strategy, with strong governance and operational decarbonisation. Its progress in climate disclosure and fleet modernisation highlights growing alignment between sustainability and long-term business resilience.

Singapore Airlines’ FY2024/25 Sustainability Report is best read as a mature aviation-sector disclosure built around regulatory convergence rather than a narrow compliance exercise. It is the Group’s 13th sustainability report, covers FY2024/25 from 1 April 2024 to 31 March 2025, and is prepared with reference to the SGX sustainability reporting rules, GRI Universal Standards 2021, and TCFD recommendations, while also serving as its Communication on Progress under the UN Global Compact. The reporting boundary is intentionally focused on the two airline businesses, SIA and Scoot, with other non-listed subsidiaries included only where relevant and material, and SIA Engineering reported separately.

That matters because airlines now sit at the intersection of several disclosure regimes at once: exchange-led climate reporting, investor demand for decision-useful ESG data, and sector-specific carbon accounting rules. SIA’s report reflects that pressure. It pairs general sustainability disclosure with aviation-specific reporting obligations such as externally verified flight emissions data for CORSIA, EU ETS, and UK ETS compliance, suggesting that climate disclosure in aviation is increasingly shaped by operational reporting systems rather than narrative-only sustainability communications.

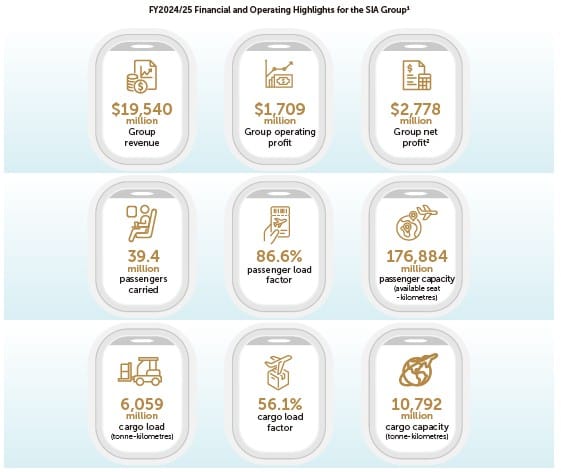

The report also signals a strategic framing of sustainability within a commercially successful year. SIA reported FY2024/25 revenue of S$19.54 billion, operating profit of S$1.709 billion, and net profit of S$2.778 billion, while carrying 39.4 million passengers across a 128-destination passenger network. That combination of strong commercial performance and expanding sustainability infrastructure is notable because it shows SIA presenting ESG as embedded in business continuity, capital allocation, and long-term competitiveness rather than as a post-profit distribution of corporate responsibility activities.

Governance architecture and accountability

The governance architecture is one of the report’s strongest features. The Board states explicitly that sustainability is integral to business operations and strategy, and oversight is distributed across several committees rather than isolated in a single ESG forum. The Customer Experience, Technology and Sustainability Committee has overall oversight of sustainability management and climate-related risks and opportunities; the Board Safety and Risk Committee handles risk governance, including operational risks arising from climate change; the Audit Committee reviews sustainability and climate reporting processes; and the Executive Committee oversees policies relating to carbon markets.

This layered approach is significant for aviation because the most material ESG issues are cross-functional by nature. Decarbonisation is not just an environmental topic; it is tied to fleet planning, regulatory exposure, finance, procurement, customer pricing, and operational resilience. SIA’s structure acknowledges that reality by linking the Sustainability Office, the Sustainability Steering Committee, and the Group Risk and Compliance Management Committee into a broader governance system chaired by senior executives and reviewed quarterly at Board-committee level.

There is also a useful governance signal in leadership design. SIA appointed its first Chief Sustainability Officer in 2023, and the report shows sustainability targets, material topics, and reporting outputs being reviewed annually by management and surfaced regularly to the Board. In practice, this suggests SIA has moved beyond a sustainability-coordination model toward a governance-embedded model where ESG is part of formal management review cycles, risk escalation channels, and Board education. For investors, that lowers the risk that the report is disconnected from decision-making.

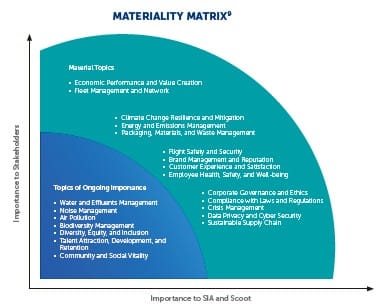

Materiality approach and risk prioritisation

SIA’s materiality process remains stakeholder-driven, but it is also fairly stable. The latest full assessment was performed in 2022 with Scoot included, and FY2024/25 management and the Board committee reaffirmed the continued relevance of 14 material topics. Those topics cover the expected aviation themes—economic performance, fleet management, climate resilience and mitigation, energy and emissions, waste, flight safety, customer experience, employee well-being, governance, cyber security, crisis management, and sustainable supply chain.

This stability can be interpreted in two ways. Positively, it suggests SIA has a relatively settled understanding of what drives value and risk in its business model. More cautiously, it means the report is still anchored in a materiality architecture built before the recent acceleration of double materiality expectations in other jurisdictions. The report clearly links stakeholder concerns, business strategy, and impact areas, but it is not yet framed in the more formal double-materiality language increasingly seen under European-style reporting logic. Even so, the content of the material topics already spans both enterprise and outward-impact lenses.

A more advanced element appears in the TCFD section. The report states that the Group strengthened its assessment of climate-related risks in FY2024/25 by establishing financial materiality thresholds and conducting quantitative scenario analysis for key risks. That is an important step because it moves climate discussion from broad narrative risk statements toward financially oriented prioritisation. In sectors like aviation, where transition costs and physical-disruption risks can both become balance-sheet issues, this kind of climate-risk quantification is increasingly central to credible disclosure.

Climate, supply chain, and social dimensions

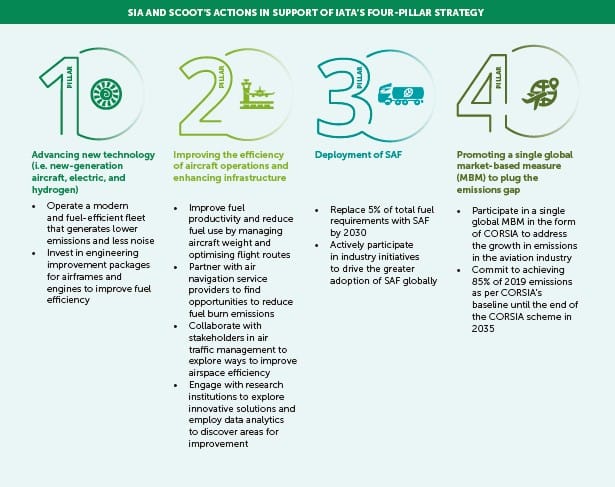

Climate is the dominant strategic ESG theme in the report, as it is for most airlines. SIA reiterates its 2050 net zero ambition and anchors it in a multi-pronged strategy: new-generation aircraft, operational efficiency, sustainable aviation fuel, and market-based measures including CORSIA. The report’s climate section is unusually explicit in showing how the Group maps its own actions to IATA’s four-pillar framework, and the chart on page 32 visually allocates the industry’s projected abatement mix across new technology, operational and infrastructure improvements, SAF, and market-based measures. That visual framing is useful because it makes clear that SIA does not present SAF as a stand-alone solution, but as part of a portfolio pathway.

The immediate decarbonisation lever remains fleet modernisation. As of 31 March 2025, the Group operated 205 aircraft with an average operating fleet age of seven years and eight months, and more than 70% of the operating fleet consisted of new-generation aircraft. SIA also says new-generation aircraft are expected to make up 90% of the fleet by 2030. In a sector where technological breakthrough timelines remain uncertain, this is a practical and commercially legible decarbonisation strategy: spend capital on the best currently available technology while keeping optionality for future fuels and propulsion pathways.

SAF is where the report becomes more policy-relevant. SIA and Scoot target SAF for 5% of total fuel requirements by 2030, aligning themselves with the AAPA collective pledge. The Group has progressed from pilot activity to actual procurement, including 1,000 tonnes of EU-RED-certified neat SAF in May 2024 and 1,000 tonnes of CORSIA-certified neat SAF in March 2025 from Neste, alongside an MoU with Aether Fuels on future supply from waste-based feedstocks. The report is clear, however, that scaling SAF depends on ecosystem coordination and policy architecture. Its support for Singapore’s Sustainable Air Hub Blueprint and participation in consultations on a SAF levy underscore that airline decarbonisation is as much a market-design challenge as an operational one.

The supply-chain dimension is therefore strategically important even though it receives less narrative prominence than climate. Sustainable supply chain management is one of the 14 material topics, and the report links poor ESG management across the value chain to exposure not only from labour and environmental risks but also from rising supply-chain emissions. Stakeholder engagement with suppliers focuses on code-of-conduct adherence, continuity planning, corrective action, and the gradual refinement of sustainable practices. That is a credible baseline, though the broader implication is that airlines will increasingly need to move from code-based supply governance toward emissions-informed supplier strategy, especially as Scope 3 expectations deepen.

On the social side, the report remains grounded in the operating realities of aviation rather than broad social claims. Flight safety and security remain material, alongside customer experience and employee health, safety, and well-being. The report also introduces more visible social-investment infrastructure, notably the Singapore Airlines Foundation with a S$30 million endowment and programmes aimed at youth uplift and aviation-career exposure. This is relevant not just as philanthropy but as talent-pipeline strategy in a sector that faces long-term workforce capability needs.

Metrics, targets, and data robustness

The report is strongest when it links operational targets to measurable indicators. On climate and resource use, it reports 17.1 million tonnes of Scope 1 emissions, 118,914 tCO2e avoided from fuel reduction initiatives, overall fleet fuel productivity of 3,851 load tonne kilometre per tonne, 28,447 MWh of total energy consumed across relevant ground assets, 5,458 MWh of renewable energy consumed in SIA-owned buildings in Singapore, and detailed waste and water metrics. This breadth is useful because it gives readers indicators across air and ground operations, even if aviation’s climate profile remains overwhelmingly flight-driven.

Some of the most decision-useful data sits in the fuel-efficiency disclosures. The report itemises avoided emissions from operational measures such as Opticlimb, statistical contingency fuel, optimal flap take-off, arrival sequencing into Singapore Terminal, and reduced reliance on auxiliary power units. Together these initiatives delivered an estimated 37,631 tonnes of fuel savings and 118,914 tCO2e avoided in FY2024/25. This level of operational granularity is stronger than many corporate sustainability reports because it shows decarbonisation not just as a capital-spending story but as an engineering and operational-discipline story.

The limitations are also visible. SAF procurement volumes remain small relative to total fuel demand, which is not surprising but is analytically important. Likewise, the report notes that quantitative climate scenario analysis currently focuses on selected Singapore assets and key risks such as precipitation-stress flooding and emissions-reporting compliance cost. That is a meaningful advance, but it still represents a partial view of climate exposure rather than a full enterprise-wide climate value-at-risk model.

Assurance, credibility, and comparability

SIA has not obtained full external assurance over the sustainability report, and that is one of the clearest boundaries on credibility. Instead, it relies on internal audit review of the sustainability reporting process and selected key indicators, with outcomes reported to the Board Audit Committee. Flight emissions data, however, does undergo external assurance for regulatory schemes including CORSIA, EU ETS, and UK ETS. In effect, the report sits in a hybrid assurance position: stronger on regulated emissions data than on the sustainability report as a whole.

That mixed picture is common in transport and aviation. It reflects a world in which the most robustly assured ESG data is often the data tied to compliance obligations, while broader sustainability disclosure still relies on internal controls and review processes. SIA’s use of external consultants for annual gap analysis, internal audit review under SGX rules, and committee-level governance over reporting does improve trustworthiness. But relative to where global reporting is heading, full or broader limited assurance would likely be the next step if SIA wants to strengthen comparability and investor confidence further.

Comparability is strengthened in other ways. The report uses GRI and TCFD indexing, quantifies targets over time, and shows the evolution of its climate-reporting journey from qualitative scenario analysis and partial Scope 3 reporting to quantitative scenario analysis and full reporting across all 15 Scope 3 categories. That trajectory matters because it indicates learning and methodological deepening, not just report expansion.

Strategic implications for the sector

For the aviation sector, the report reinforces a central reality: credible transition planning is increasingly inseparable from fleet strategy, fuel procurement capability, and policy engagement. SIA’s report does not claim that it can decarbonise through internal action alone. Instead, it openly situates progress within industry coordination, government action, supplier development, and carbon-market rules. That is analytically useful because it reflects the true structure of aviation decarbonisation rather than overstating company-level control.

The report also shows that premium aviation brands are increasingly using sustainability to defend operational resilience and network advantage, not just reputation. Fleet modernity, digital capability, customer data governance, and multi-hub strategy all appear here as parts of long-term resilience. The implication is that, in aviation, ESG maturity may increasingly correlate with balance-sheet strength and strategic optionality, because the transition requires capital, technological experimentation, and regulatory responsiveness.

ESG maturity and future positioning

Overall, SIA appears to be in an advanced but transitional stage of ESG maturity. It has strong governance architecture, long-running reporting practice, operationally grounded climate disclosure, and improving climate-risk analysis. It also shows a relatively sophisticated understanding of how commercial strategy, technology investment, and decarbonisation interact. The report’s strongest feature is that it treats sustainability as part of airline-system management rather than a separate CSR stream.

The next phase will likely depend on depth rather than breadth. The report already covers the expected topics; the future question is whether SIA can deepen disclosure on financially material climate pathways, transition-cost sensitivities, supply-chain decarbonisation, and broader external assurance. If it can, it will be better positioned not only for regulatory evolution in Singapore and abroad, but also for a market environment in which capital providers increasingly look for evidence that transition readiness is operationally real and economically legible.

Pacifica ESG View

Singapore Airlines’ FY2024/25 Sustainability Report presents a credible picture of an airline moving from structured ESG management toward more transition-oriented disclosure. Its governance architecture is strong, its climate narrative is operationally grounded, and its reporting maturity is evident in the progression from qualitative to quantitative climate assessment and from partial to full Scope 3 category coverage. The report is less compelling where assurance remains partial and where enterprise-wide financial implications of transition are still only selectively quantified. Even so, it stands out for treating decarbonisation as a systems challenge involving fleet renewal, SAF market building, regulatory engagement, and operational discipline, rather than as a single-technology solution.

Implications for the wider market

The wider lesson is that hard-to-abate sectors are entering a phase where ESG credibility will depend less on target setting alone and more on the ability to demonstrate implementation pathways, regulatory preparedness, and capital-backed transition choices. SIA’s report shows how that can look in practice: climate strategy linked to fleet and fuel decisions, governance embedded across committees, and risk disclosure gradually becoming more financially oriented. For other airlines and transport operators, the benchmark is shifting. Broad commitments are no longer enough; stakeholders increasingly expect evidence of execution, scenario-based risk thinking, and disclosure systems that can support both sustainability reporting and regulated carbon compliance.