CLP Holdings 2025 Sustainability Report Analysis: Navigating the Energy Transition Through Climate, Nature and Resilience

CLP Holdings’ 2025 Sustainability Report highlights its progress on decarbonisation, climate governance and supply chain resilience. This analysis examines the company’s transition strategy, disclosure maturity and readiness for an increasingly regulated ESG landscape.

CLP Holdings’ 2025 Sustainability Report reflects a utility group operating in a disclosure environment that is moving rapidly from voluntary ESG reporting toward investor-oriented sustainability disclosure. The report is positioned alongside CLP’s Annual Report, ESG Databook, Materiality Assessment Report and Climate Vision 2050, indicating that sustainability information is no longer treated as a standalone communications exercise but as part of a broader corporate reporting architecture.

A notable feature is CLP’s stated alignment with HKFRS S1 and compliance with HKFRS S2, both of which are fully aligned with the ISSB standards. This is important for Hong Kong-listed issuers because climate-related disclosure under the HKEX ESG Reporting Code is entering a more demanding phase. CLP’s early adoption gives the market a practical example of how a large infrastructure-heavy issuer can separate financially material sustainability information in the annual report from impact-focused disclosures in the sustainability report.

The company also references GRI, SASB, TNFD and sector-specific electric utility guidance. This multi-framework approach improves comparability but also raises the complexity of report navigation. CLP has responded by creating a separate ESG Databook and ESG Data Hub, which helps users access quantitative data without overloading the narrative report.

Governance architecture and accountability

CLP’s governance model is relatively mature compared with many listed companies in the region. The Board retains overall responsibility for sustainability and business strategy, while the Sustainability Committee and Audit & Risk Committee provide complementary oversight. The Sustainability Committee focuses on sustainability matters, while the Audit & Risk Committee covers risk management, internal control and assurance of ESG data.

At management level, the Sustainability Executive Committee is chaired by the CEO and was expanded in 2025 to include all members of the Group Executive Committee. This is a meaningful governance enhancement because sustainability decisions in utilities are highly cross-functional, involving strategy, finance, operations, procurement, digital systems, human resources and regional business units. CLP also states that the CEO and CFO jointly sign off the General Representation Letter connected with ESG assurance, which strengthens management accountability for non-financial data.

The Group Sustainability Department plays a coordinating role across climate action, sustainability disclosure, ESG performance management and emerging issues such as human rights and procurement. This structure suggests that CLP is moving beyond “reporting ownership” toward operational integration. The main challenge is whether governance oversight continues to translate into measurable execution, particularly in coal phase-out, safety performance, supplier risk management and climate transition financing.

Materiality approach and risk prioritisation

CLP applies a double materiality approach within a structured three-year cycle. In 2025, it implemented the second year of this cycle, building on stakeholder interviews and refreshing previous results. Financially material topics are addressed in the Annual Report, while impact material topics are covered in the Sustainability Report.

This distinction is important. For investors, financially material issues include climate-related physical and transition risks, capital allocation, asset values and regulatory exposure. For broader stakeholders, impact materiality covers the company’s effects on people, communities, ecosystems and the economy. CLP’s approach therefore reflects the direction of both European-style impact reporting and ISSB-style enterprise value reporting, even though the two perspectives are not identical.

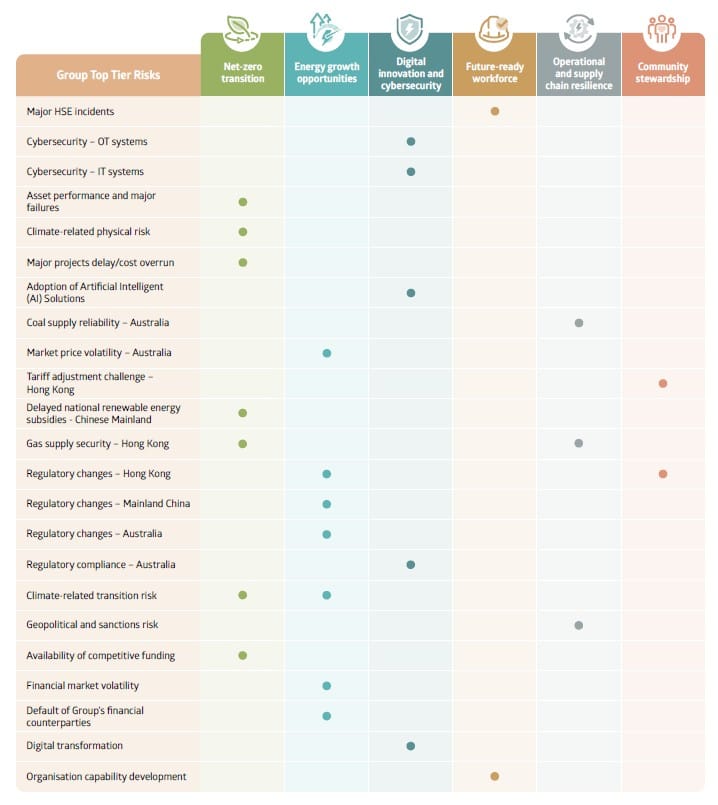

CLP’s six material sustainability topics are net-zero transition, energy growth opportunities, digital innovation and cybersecurity, future-ready workforce, operational and supply chain resilience, and community stewardship. These topics are closely connected to its top-tier risks, including climate-related physical risk, climate-related transition risk, gas supply security, regulatory changes, cyber risks and major health, safety and environment incidents. The materiality process appears robust, but the report would be stronger if it provided clearer ranking logic between topics and showed how materiality outcomes directly affect capital expenditure or asset-level transition decisions.

Climate, supply chain, and social dimensions

Climate remains the central ESG issue for CLP because the group still has material exposure to fossil fuel generation while also investing in renewable energy, nuclear, gas, storage, smart meters and energy services. CLP reports a Group greenhouse gas emissions intensity of 0.50 kg CO₂e/kWh in 2025, down from 0.53 kg CO₂e/kWh in 2024 and 21% lower than the 2019 baseline. Its 2030 target is 0.26 kg CO₂e/kWh, implying that further reductions will require continued portfolio transformation, not only operational efficiency.

The company maintains a commitment to phase out coal-fired power generation before 2040. It also reports that absolute Scope 3 Category 11 emissions have decreased by 35% against the 2019 baseline, already exceeding the 2030 reduction target of 28%. However, for a utility, Scope 3 performance can be influenced by portfolio changes, asset accounting boundaries and downstream use assumptions. Users should therefore read this figure alongside the ESG Databook and future assurance statements.

Supply chain sustainability is becoming more strategic. CLP’s three-year Sustainable Procurement Roadmap focuses on supplier awareness, compliance, priority management, impact and stakeholder recognition. The company reports that more than 3,800 suppliers have acknowledged its Supplier Code of Conduct, against a 2026 target of over 4,000. This is a positive foundation, although acknowledgement is not equivalent to verified performance. The next stage of maturity will depend on risk-based supplier assessments, corrective actions, traceability and integration of human rights due diligence.

Social issues are addressed through workforce development, diversity, safety and community programmes. CLP reports that women held 31.6% of leadership roles, Board female representation reached 38%, and 17.7% of training hours were dedicated to upskilling and reskilling. However, the report also discloses several fatal incidents, including traffic incidents and fatalities connected with contractor or investment-related operations. This creates a necessary balance in the ESG narrative: strong systems and targets exist, but safety performance remains an area requiring continuous oversight.

Metrics, targets, and data robustness

CLP’s report is data-rich and target-oriented. Key environmental targets include reducing greenhouse gas emissions intensity by 59% to 0.26 kg CO₂e/kWh by 2030, achieving net-zero greenhouse gas emissions across the value chain by 2050, and phasing out coal before 2040. It also reports progress against air emissions, waste and freshwater targets.

On customer-side transition, the company reports more than 2.88 million smart meters connected in Hong Kong since 2018, around 48 GWh of electricity savings from over 600 buildings under the Eco Building Fund, and around 48 GWh of electricity savings from more than 600 energy audits. These metrics are important because utilities increasingly need to demonstrate not only how they decarbonise supply, but also how they enable customers to reduce demand and electrify operations.

CLP also discloses digital and innovation metrics, including 39 deployed use cases of innovative technologies, exceeding its target of 28. The report’s discussion of ERP transformation, AI, data analytics and cybersecurity reflects a broader trend: sustainability performance increasingly depends on data architecture. However, the report would benefit from clearer disclosure on data quality controls, system boundaries and estimation uncertainty, especially for Scope 3 emissions, supplier metrics and nature-related indicators.

Assurance, credibility, and comparability

CLP’s credibility is supported by multiple reporting frameworks, Board-level oversight and independent assurance over selected ESG data. The Audit & Risk Committee is responsible for ensuring appropriate assurance of materiality assessment and ESG data, and the report states that findings are presented to management and the Board. This is important as Hong Kong moves toward a more formal sustainability assurance regime aligned with HKSSA 5000 and ISSA 5000.

The report also discusses evolving assurance standards, including ISSA 5000 and HKSSA 5000. This demonstrates readiness for a market where sustainability information will increasingly be treated with the same discipline as financial information. For investors, this is valuable because energy transition claims, emissions metrics and climate risk disclosures are only useful if the underlying data systems are reliable.

Comparability remains a challenge. CLP operates across Hong Kong, Mainland China, Australia, India and other markets, with different regulatory systems, fuel mixes, ownership structures and accounting boundaries. Portfolio changes can affect year-on-year performance. For this reason, the ESG Databook and clear boundary explanations are essential for analysts seeking to distinguish operational improvement from changes in asset scope.

Strategic implications for the sector

CLP’s report illustrates how the power sector is becoming a test case for integrated sustainability disclosure. Utilities face simultaneous pressure to decarbonise, maintain reliability, preserve affordability, manage capital intensity, address nature and community impacts, and digitise grid infrastructure. These pressures cannot be managed through climate targets alone.

The inclusion of TNFD-aligned nature discussion is especially relevant. Power generation, transmission infrastructure, cooling water use, land occupation and renewable energy development all have nature-related dependencies and impacts. CLP’s forest restoration programme with Kadoorie Farm & Botanic Garden provides a concrete biodiversity initiative, but the strategic question is broader: how nature-related risk assessment will be integrated into asset planning, project development and procurement.

For other utilities, CLP’s reporting approach suggests that future ESG leadership will require three capabilities. First, companies need climate transition plans linked to capital allocation. Second, they need data systems that can support assured sustainability information. Third, they need governance structures that connect Board oversight with operational decision-making across regions and business units.

ESG maturity and future positioning

CLP’s 2025 Sustainability Report demonstrates a high level of ESG reporting maturity, particularly in framework alignment, governance structure, climate target disclosure and stakeholder-oriented reporting. The company has moved beyond basic compliance and is positioning sustainability as part of long-term business resilience.

At the same time, the report shows that the energy transition remains operationally difficult. Coal phase-out, gas transition, hydrogen pilots, renewable expansion, customer electrification and affordability must be managed together. Safety incidents and supply chain human rights risks also remind readers that ESG maturity is not only about disclosure sophistication; it is about performance under complex operating conditions.

Looking forward, CLP’s future positioning will depend on whether it can translate strong reporting architecture into measurable transition outcomes. Investors will likely focus on emissions intensity trajectory, coal retirement progress, renewable and storage investment, regulated return implications, climate risk quantification and assurance readiness. Stakeholders will also expect stronger evidence of just transition, contractor safety, supplier accountability and nature-positive planning.

Pacifica ESG View

CLP’s 2025 Sustainability Report is one of the more advanced examples of utility-sector ESG disclosure in Asia. Its strengths lie in HKFRS S1/S2 readiness, Board and executive-level accountability, double materiality, climate transition reporting, and structured ESG data presentation. The report is credible because it discloses both progress and difficult issues, including safety incidents and ongoing fossil fuel exposure. The key area to watch is execution: whether CLP can sustain emissions reductions, phase out coal, strengthen supplier due diligence and integrate nature-related risks into business planning. Overall, the report reflects a company with mature ESG governance, but still operating within a hard-to-abate and highly regulated sector.

Implications for the wider market

CLP’s report signals where sustainability reporting in Hong Kong and Asia-Pacific is heading. Large issuers will increasingly need ISSB-aligned climate disclosure, clearer financial effects of climate risks, stronger ESG data systems and assurance-ready controls. For utilities and infrastructure companies, climate disclosure alone will not be enough; investors will also expect transition plans, supply chain resilience, safety governance, nature-related assessment and credible social safeguards. CLP’s approach provides a useful reference point, but it also shows that reporting maturity must be matched by operational performance. The wider market should treat this as a benchmark for disclosure structure, while recognising that future scrutiny will focus more heavily on verified outcomes.